Baby boomers (those born between 1946 and 1964) now constitute 40 percent of the U.S. population, controlling 67 percent of the nation’s wealth.

Wealth management products are available, but many do not focus on innovative data visualization, are often desktop-based, and do not incorporate persuasion to change behavior. Mobile solutions face the additional challenge that many baby boomers are not as familiar with mobile devices as younger people.

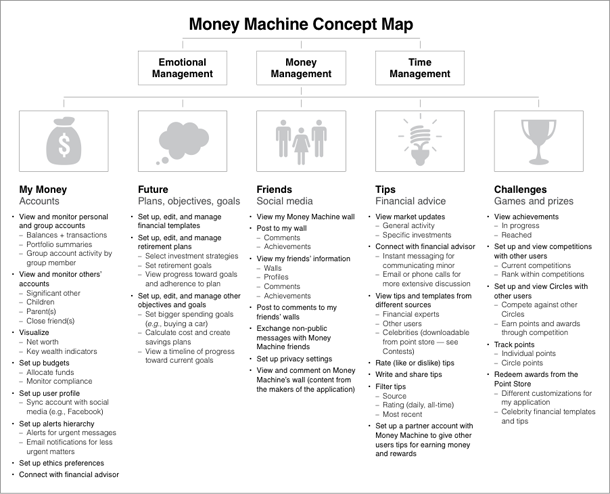

The author’s firm, AM+A developed a concept design called the Money Machine, to answer two critical questions:

- How can information visualization and design promote change in wealth-management behavior? In general, we sought to assist people by enabling them to make decisions wisely about spending and saving appropriately. A specific example might involve managing the finances of an elderly parent with contributions coming from several different family members.

- How can mobile technology assist in presenting persuasive information to promote behavior change? In general we sought to enable people to review their “dashboard” easily, connect with specific family and friends who might be able to advise or contribute, and to provide incentives and game-like attributes that would make wise actions more appealing to carry out.

Market Research, Personas, and Use Scenarios

Following the philosophy of user-centered design, we conducted qualitative research to understand the target market and distributed a questionnaire that explored smartphones and social media, money management, technology and money, and demographics.

We used the detailed results of the questionnaire to establish a set of five personas, and used the questionnaire results, as well as these personas, to construct specific use scenarios describing financial monitoring, security, social media, and gamification.

Competitive Products Research

We studied approximately twenty financial and wealth management websites and iPhone applications (including Ameritrade, iBank, and Mint.com). Through screen comparison analysis and customer review analysis, we derived benefits and drawbacks of the applications, such as how easy it was to enter and track information, how flexible financial information formats were, and whether they had integrated mobile and web versions. Noting that few of these applications included much content related to actual behavior change, and that most addiction treatment programs (seeking to change behavior) do include such components, we concluded that usable, useful, and appealing UI design for wealth management should include incentives to prompt behavior change. These additional components go far beyond simply displaying information.

Desirable Characteristics

Based on our review of current products, the statement of needs and expectations of the interviewees, and knowledge gained from a previous, similar effort (called the Green Machine), we came to some general conclusions about desirable characteristics of the Money Machine. A good wealth management application should help users set goals, provide dynamic charts and illustrations, host competitions, and provide step-by-step instructions to motivate behavior change.

Extensive, up-to-date, user-friendly, and flexible searchable databases are another priority. Similarly, the Money Machine must liberate users from cumbersome manual data entry, furnishing a varied data entry system (for example, document or database scanning).

The Money Machine must also encourage and strengthen team-oriented behavior change. Cooperation and competition within and among teams can encourage greater restraint and financial control. Virtual rewards (for example, “star” designations) provide strong motivation, and real financial rewards can prompt a significant change in behavior.

Last but not least: The Money Machine should be fun. Gamification provides a further incentive for users to learn about selecting wise investment/expenditure combinations, and controlling risk efficiently and effectively. The Money Machine should allow users to share these experiences, primarily through Facebook, Twitter, and blogs.

Use of Persuasion Theory

We sought to combine information design with persuasion design to change people’s behavior. Based on Fogg’s behavior model for persuasive design, and Cialdini’s theories of persuasion, we defined five key processes to create behavioral change:

- Increase frequency of use

- Motivate changing some living habits (save, plan, invest)

- Teach how to change living habits

- Persuade users to plan short-term change

- Persuade users to plan long-term change.

We also adapted Maslow’s analysis of fundamental human needs to the Money Machine context:

- The safety and security need is met by the ability to visualize the amount of expense saved

- The belonging and love need is met by the ability to share with, and gain support from, friends and family

- The esteem need is satisfied by social comparisons that display improvement in financial control and skill, as well as by self-challenges that display goal accomplishment

- The self-actualization need is fulfilled by the ability to visualize improvement of financial indexes and mood, and to predict change in users’ future economic scenarios.

Increasing Frequency of Use

Game-like attributes and award concepts typically increase frequency of use of applications. Users might be given virtual rewards, as well as real money contributed by government or financial institutions, for use of the application.

Increasing Motivation

Users’ potential financial conditions are an important incentive for behavior change. Viewing their current versus predicted economic status over the next twenty to thirty years gives users greater understanding of the strengths and weaknesses of their financial strategy.

Because setting goals improves learning outcomes and provides quantitative performance data, the Money Machine asks users to set time-based goals for spending reduction, savings, and retirement. To achieve each goal, users receive suggested step-by-step action plans.

In addition, we created ten monthly challenges. In meeting them, users can make short-term behavior changes that will generate long-term positive impacts.

Social interaction also motivates behavior change through community support and informal competition or comparison. Users can form groups of family and friends and participate in competitions. Although based around financial controls and exercises, users need not reveal personal financial data.

The Money Machine also leverages social networking by integrating features found in forums, blogs, Facebook, and Twitter.

Improving Learning

Understanding long-term wealth management is crucial. To improve learning, the Money Machine integrates contextual tips on:

- Wiser consumption

- Increased financial control

- Tackling complications associated with debt and poor investments

- Coping with principle burn rates that are either too high or too low.

We sought to make the education process entertaining as well as informative. Proposed games teach users to choose the right proportion of investments.

Next Steps

We plan to develop a working prototype to conduct user evaluations, validate personas, and use scenarios, then revise the information architecture and the look-and-feel appropriately. We also are interested in researching and developing improved information visualizations and considering how the Money Machine might be redesigned for different cultures and for enterprise use, not only individual consumer use.

In general, we plan to test whether the application can persuade people to exercise greater fiscal control, adopt healthier wealth management habits, and pursue a more financially sound lifestyle under real use conditions over the long term. If the design philosophy about adding persuasion characteristics to information display in order to change behavior is proven correct, this approach could have significant wealth-management benefits.

and used by others. Selecting a group account member from the top bar displays the total money in the account, versus that member’s contributions and expenses for a given timeframe.

文章全文为英文版머니 머신 프로젝트는 “베이비 붐 세대”를 위한 자산 관리 태도를 향상하기 위한 효과적인 방법을 연구, 분석, 디자인 그리고 평가합니다. 본 프로젝트는 사람들이 훌륭한 디자인의 모바일 스마트폰과 태블릿 애플리케이션을 통해 그들의 자산 소비를 감소하고 지급 가능한 자금의 수명을 증가하도록 설득하고 동기 부여를 하는 것입니다. 머니 머신 콘셉트 디자인은 정보 디자인과 시각화를 설득 디자인과 조화합니다. 본 논문은 머니 머신의 사용 인터페이스 개발, 정보 디자인, 정보 시각화 및 설득 디자인 사용 등을 설명합니다. 결과를 소개하고 연구와 개발의 다음 단계를 제시하기도 합니다.

The full article is available only in English.O projeto Máquina de Dinheiro pesquisou, analisou, projetou e avaliou formas poderosas de melhorar o comportamento da gestão de riquezas para “baby boomers”. O projeto pretende persuadir e motivar as pessoas a reduzirem seu consumo de ativos e aumentar a longevidade dos fundos disponíveis por meio de aplicativos móveis para tablet e smartphone bem projetados (com um portal da web associado). O projeto conceitual da Máquina de Dinheiro combina design de informações e visualização com design de persuasão. Este artigo explica o desenvolvimento da interface com o usuário da Máquina de Dinheiro, design de informações, visualização de informações e o uso do design de persuasão. Ele apresenta os resultados e considera as próximas etapas de pesquisa e desenvolvimento.

O artigo completo está disponível somente em inglês.マネーマシーン(Money Machine)プロジェクトは、「団塊世代」の資産管理に関する行動様式を改善する強力な方法について、調査、分析、デザイン、評価を行った。このプロジェクトでは、資産の消費を削減し、利用できる資金が長持ちするように、よく考えられたデザインのスマートフォンおよびタブレット用アプリケーションを(関連したウェブポータルと共に)提供し、ユーザを説得し、動機付けすることを意図している。マネーマシンのコンセプトデザインは、情報デザインと説得的デザインを使った視覚化の組み合わせから成る。この記事では、マネーマシーンのユーザインタフェースの開発、情報デザイン、情報視覚化、そして説得的デザインについて解説する。また、プロジェクトの結果を紹介し、研究開発上の次のステップへの考察を行っている。

原文は英語だけになりますEl proyecto The Money Machine (La Máquina del Dinero) estudió, analizó, diseñó y evaluó formas eficaces para mejorar la gestión del patrimonio en la generación de la posguerra. El proyecto busca persuadir y motivar a la gente para que reduzca el consumo de activos y aumente la longevidad de los fondos disponibles mediante una bien diseñada aplicación móvil para teléfonos inteligentes y una para tabletas (con un portal web asociado). El diseño conceptual de The Money Machine combina el diseño de información y la visualización con el diseño persuasivo. En este artículo se explica el desarrollo de la interfaz de usuario de The Money Machine, el diseño de la información, la visualización de la información y el uso del diseño persuasivo. Exhibe los resultados y tiene en cuenta los próximos pasos de investigación y desarrollo.

La versión completa de este artículo está sólo disponible en inglés.